If your business depends on wheels, you already know that driving for work is nothing like driving for pleasure. Making deliveries, hauling equipment, or shuttling clients changes everything. One wrong move on a rainy Tuesday afternoon could put your entire company at risk. That is why asking for a business vehicle insurance quote is one of the smartest things you can do as an owner.

But here is where people get tripped up. Many assume their personal car insurance will cover them while they are on the clock. That assumption can be expensive. Personal policies almost always exclude commercial activity. Whether you are dropping off office supplies or transporting heavy machinery, if an accident happens during work hours, your personal coverage may say no. You could be left paying hospital bills and repair costs from your own pocket. That is a nightmare no business owner wants to face.

Getting a proper business vehicle insurance quote changes the game. It gives you coverage designed specifically for work-related driving. It accounts for higher mileage, multiple drivers, valuable cargo, and the unique risks your industry faces. This guide will walk you through everything from what goes into a quote to how you can get the best possible rate without cutting corners on protection.

What Does a Business Vehicle Insurance Quote Actually Include?

When you request a business vehicle insurance quote, you are asking an insurance company to calculate your risk and tell you what they would charge to cover it. Unlike a personal quote that only looks at your car, driving record, and home address, a commercial quote digs much deeper.

The insurer wants to know about your vehicles, sure. But they also want to know about your drivers, the kind of work you do, how far you travel, what you carry, and even where you park at night. Every detail matters. A business vehicle insurance quote reflects the unique exposure of your operation. That means two florists with identical vans could get completely different quotes if one delivers only locally and the other drives three hundred miles each day.

The final number you see is not random. It comes from years of data about how often commercial vehicles crash, what claims cost, and which industries present the most danger. Understanding that helps you see the quote for what it is, a risk assessment, not just a price tag.

Why Personal Auto Policies Leave You Exposed

Let me be direct. Using your personal insurance for business driving is like wearing a raincoat full of holes. You think you are protected, but the first real storm proves you wrong. Every standard personal auto policy contains language that excludes coverage when the vehicle is used for business purposes.

What counts as business purposes? Delivering goods for a fee, transporting paying passengers, hauling tools to a job site, even running to the bank with your daily deposit. If the activity generates income or supports your trade, it is business. And personal policies do not like business.

If you crash while making a delivery and the insurer investigates, they will ask one question. Were you working? If the answer is yes, they can deny your claim entirely. That means no help with vehicle repairs, no medical payments, and no liability defense if someone sues you. Your personal policy simply walks away.

A business vehicle insurance quote solves this problem by providing coverage that actually matches what you do. It includes higher liability limits, protection for cargo, and options for hired and non-owned vehicles. It is the right tool for the job.

What Factors Shape Your Business Vehicle Insurance Quote

Insurers look at a long list of details when putting together your business vehicle insurance quote. Knowing what they care about gives you the power to improve your rates before you even call an agent.

Your Vehicles

The cars and trucks you drive matter a lot. A heavy box truck costs more to insure than a small sedan because it can cause more damage in a crash. Expensive vehicles cost more to repair or replace. Older vehicles might lack modern safety features. When you request a business vehicle insurance quote, have your vehicle identification numbers, makes, models, and years ready.

Your Drivers

Every person who gets behind the wheel of a company vehicle influences your quote. Insurers run motor vehicle reports on each driver. A clean record with no tickets or accidents helps you get a lower rate. A driver with multiple speeding violations or a DUI will raise your quote significantly. Some insurers may even refuse to cover certain high-risk drivers. It pays to be selective about who drives for your business.

Your Industry and Cargo

What do you haul? Construction materials, food products, medical supplies, or hazardous waste? Each type of cargo carries different risks. Carrying dangerous goods drives up your business vehicle insurance quote because a spill or fire could cause massive damage. Even carrying valuable items like electronics increases risk because thieves target those vehicles. Be honest about your cargo, because hiding it will only hurt you later.

Your Mileage and Territory

Driving more miles means more chances to crash. That is simple math. A business vehicle insurance quote will ask for annual mileage estimates for each vehicle. If you drive fifty thousand miles a year across multiple states, expect to pay more than a business that drives ten thousand miles within one city. Urban driving also raises rates because traffic congestion leads to frequent fender benders.

Your Claims History

Past behavior predicts future risk, at least in the eyes of insurers. If your business has filed several claims in the last few years, your quote will be higher. On the flip side, a clean claims history makes you attractive to insurers. They may offer lower rates to win your business. If you have gone three or more years without an accident, make sure to mention that when requesting your business vehicle insurance quote.

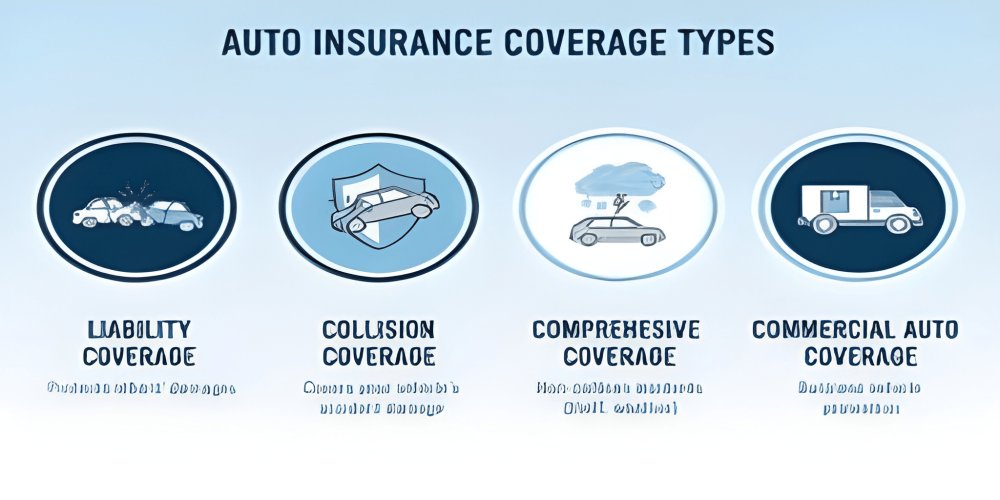

Coverage Types You Need to Understand

Not all business vehicle insurance quotes include the same protections. Some agents strip away valuable coverages to offer a low price. Then when you have an accident, you discover the gap. Here are the key coverages to look for.

Liability Insurance

This is the backbone of any commercial auto policy. Liability pays for injuries and property damage you cause to others in an at-fault crash. If you rear-end a luxury SUV and send the driver to the hospital, liability coverage responds. For most businesses, experts recommend at least one million dollars in liability protection. State minimums are almost never enough for commercial operations.

Physical Damage Coverage

This covers your own vehicles. Collision coverage pays for damage from accidents. Comprehensive coverage pays for theft, fire, vandalism, hail, or hitting an animal. If you lease or finance your vehicles, the lender will require physical damage coverage. Even if you own your vehicles outright, skipping this coverage means paying out of pocket for repairs or replacement after a loss.

Medical Payments

No matter who caused the accident, medical payments coverage helps pay for your passengers’ hospital bills. Ambulance rides, emergency room visits, and follow-up care add up fast. Adding this to your business vehicle insurance quote is usually inexpensive and provides real peace of mind.

Uninsured Motorist Coverage

Not everyone on the road carries insurance. If one of your drivers gets hit by an uninsured motorist, who pays the medical bills? Uninsured motorist coverage steps in to fill that gap. Given how many drivers lack insurance, this is a smart addition to any business vehicle insurance quote.

Hired and Non-Owned Auto Coverage

This one confuses many owners, but it is critically important. Hired and non-owned auto coverage protects your business when employees use vehicles you do not own. For example, if an employee runs a work errand in their personal car and causes an accident, your business could be sued. This coverage responds. Always ask whether a business vehicle insurance quote includes this protection.

Cargo Coverage

Standard auto insurance does not cover the goods you are hauling. If your van is stolen with ten thousand dollars worth of electronics inside, you need separate cargo coverage to recover that loss. Any business that transports inventory, tools, or products for clients should add cargo coverage to their quote.

How to Get Accurate Quotes Without the Runaround

Requesting a business vehicle insurance quote does not have to be painful. Follow these steps and you will save time and money.

Organize Your Information First

Before you call anyone, write down everything you need. Vehicle identification numbers, license plate numbers, estimated annual mileage for each vehicle, driver names and license numbers, and a description of your daily operations. Having this ready means you can get accurate quotes in one phone call rather than playing phone tag for a week.

Talk to Multiple Insurers

Do not fall in love with the first company you call. Reach out to at least three or four different providers. Include national carriers, regional insurers, and at least one independent agent. Independent agents can shop your information to multiple underwriters at once and bring back several business vehicle insurance quotes for you to compare.

Compare More Than Price

When the quotes come in, look beyond the bottom number. Check the liability limits, the deductible amounts, and the list of exclusions. A quote that looks cheap might have a ten thousand dollar deductible or exclude coverage for certain drivers. Make sure you are comparing apples to apples.

Ask About Discounts

Insurers do not always volunteer discount information. You have to ask. Common discounts include safe driver programs, telematics devices that track driving behavior, bundling with general liability insurance, paying the full annual premium upfront, and installing anti-theft devices on your vehicles. Each discount chips away at your business vehicle insurance quote.

Check the Insurer’s Reputation

A low rate means nothing if the company fights every claim. Look up customer reviews and check financial ratings from agencies like AM Best. You want an insurer that pays claims fairly and quickly. A slightly higher quote from a reputable company is better than a cheap policy from a carrier that disappears when you need them.

Mistakes That Will Cost You

People make the same errors over and over when shopping for commercial auto coverage. Learn from their mistakes.

Lying About Mileage

Some owners think they can get a lower business vehicle insurance quote by understating how many miles they drive. Insurers audit mileage. If they catch the discrepancy, they can cancel your policy or deny a claim. Just be honest.

Forgetting to List a Driver

If you have a part-time driver or a seasonal helper who sometimes takes the wheel, list them on the policy. An unlisted driver who causes a crash could leave you without coverage. It is not worth the risk.

Choosing the Cheapest Liability Limits

State minimum liability limits are dangerously low for most businesses. A single accident with serious injuries can easily exceed those limits. Your business assets, including your bank accounts and property, could be seized to pay the difference. Buy higher limits than the law requires.

Skipping the Exclusions Page

Every insurance policy has a list of things it will not cover. Common exclusions include racing, intentional damage, ridesharing, and transporting certain hazardous materials. Read that page carefully before you sign. If something is unclear, ask your agent to explain it.

Industry by Industry: What Different Businesses Face

Your business vehicle insurance quote will look different depending on your line of work.

Construction and Contractors

These businesses face high risk because they haul heavy equipment, tow trailers, and work in crowded job sites. Backing accidents are common. Theft of tools is a constant threat. Look for quotes that include tool coverage and on-hook towing liability.

Delivery and Courier Services

Driving against the clock in busy urban areas drives up claims frequency. Delivery drivers are often rushed, which leads to crashes. Insurers classify this as high-risk, so your business vehicle insurance quote will be higher. Using telematics to prove safe driving can help lower your rate over time.

Sales and Professional Services

Salespeople driving to client meetings have lower physical damage risk than freight haulers. Their quotes tend to be more affordable. However, they still need robust liability coverage and hired and non-owned auto protection for those times they use personal cars.

Farming and Agriculture

Farm vehicles split time between public roads and private land. That creates a unique risk profile. A standard business vehicle insurance quote may not fit. You might need specialized agricultural endorsements for crop transport and field operations.

Ways to Lower Your Quote Without Losing Protection

You can reduce your business vehicle insurance quote through smart practices, not just by cutting coverage.

Train Your Drivers

Insurers love businesses that invest in safety. Formal defensive driving courses, distracted driving workshops, and vehicle inspection training show that you take risk seriously. Present completion certificates to your agent and ask for a safe driver discount.

Install Tracking and Security Devices

GPS tracking devices help recover stolen vehicles. Steering wheel locks deter thieves. Security cameras in parking areas reduce vandalism claims. Each of these measures can lower your business vehicle insurance quote because they reduce the chance of a loss.

Raise Your Deductible

Increasing your physical damage deductible from five hundred to one thousand or two thousand dollars can lower your premium noticeably. Just make sure you have the cash set aside to pay that higher deductible if something happens.

Bundle Your Policies

If you buy commercial auto insurance from the same company that provides your general liability or property insurance, you will likely receive a bundling discount. Ask each insurer how much you could save by moving all your business coverage to them.

Frequently Asked Questions

This section answers the most common questions people have about business vehicle insurance quotes.

What exactly is a business vehicle insurance quote?

It is an estimate from an insurance company showing how much they would charge to cover your work vehicles and drivers. It is not a binding contract. The final price may change if the underwriter finds new information during the application process.

How long does a business vehicle insurance quote stay valid?

Most quotes are good for thirty days. Some insurers reduce that to fifteen days if market conditions are changing. If you wait longer than a month, ask for a fresh quote to ensure accuracy.

Can I get a business vehicle insurance quote if I only have one van?

Absolutely. Many small businesses, from caterers to plumbers, need coverage for a single vehicle. Insurers write policies for fleets of any size, from one vehicle to hundreds. Do not assume you need a large operation to qualify for commercial coverage.

Does a standard business vehicle insurance quote cover employees using their own cars?

No, it does not. Standard commercial auto policies cover only vehicles your business owns. To protect your company when employees run errands in their personal cars, you must add hired and non-owned auto liability coverage. Ask for it specifically.

What information must I provide to get an accurate quote?

You need vehicle identification numbers, makes, models, and years for each vehicle. You need the full name, date of birth, and driver’s license number for every employee who will drive. You also need your federal tax ID number, a description of your business, and annual mileage estimates.

How can I tell if a business vehicle insurance quote is legitimate?

Work only with licensed agents or directly with well-known insurance websites. Check that the insurer is registered with your state’s department of insurance. Be very cautious of quotes that seem far lower than others you have received. If it looks too good to be true, it probably is.

Will a recent claim increase my next business vehicle insurance quote?

Almost certainly. An at-fault accident or a theft claim will cause your rates to rise for three to five years, depending on the insurer. To minimize the damage, ask about accident forgiveness, though it is less common on commercial policies than personal ones.

How quickly can I get a business vehicle insurance quote?

For a simple business with a couple of vehicles and clean driver records, you can receive a quote within a few hours or by the next business day. For complex fleets with many drivers or a poor claims history, expect three to five business days as underwriters review the details manually.

Final Thoughts

Getting the right business vehicle insurance quote takes a little effort, but that effort pays off. You protect your company from financial disaster. You gain peace of mind every time one of your drivers heads out on the road. And you avoid the rude shock of a denied claim after an accident.

Do not rush the process. Gather your information carefully. Talk to several insurers. Read the policy details before you sign. And remember that the cheapest quote is rarely the best value. Look for the right balance of price, coverage, and company reputation.

Leave A Comment

0 Comment