A fixed deposit (FD) is one of the oldest and safest investment instruments in India: you deposit a lump sum for a fixed tenure with a bank, and at the end — or at regular intervals — you receive interest at a predetermined rate. The appeal of FDs lies in their stability: the interest rate is locked when you deposit, and unlike market-linked products (stocks, mutual funds), the returns don’t fluctuate with market volatility.

Reserve Bank of India (RBI) policy rates, inflation, macroeconomic conditions, and competition among banks influence FD rates across the banking sector. In this scenario, ICICI Bank remains a popular and widely used choice — especially for individuals seeking moderate, predictable returns on idle surplus funds or small-to-medium savings for medium-term goals.

Given India’s economic environment and rising cost of living, locking money in a risk-free instrument like an FD with decent interest remains relevant — albeit with due attention to interest rates, tenure, tax implications and inflation.

Current ICICI Bank FD Interest Rates (2025)

As of late 2025, for deposit amounts below ₹3 crore, ICICI Bank offers the following approximate interest-rate ranges (for domestic, NRO, NRE deposits) depending on tenure and the depositor’s age category. (ET Money)

Rate Range Overview

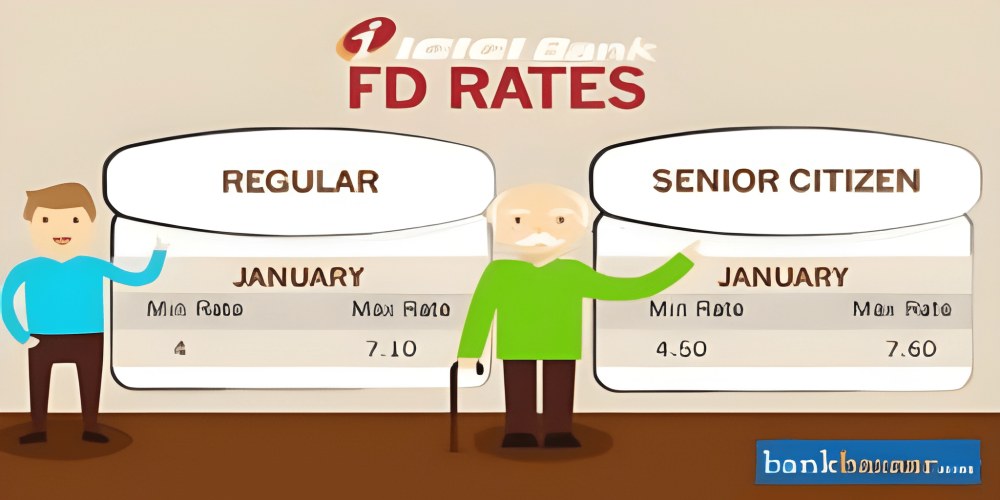

- For general customers (regular adults): interest rates vary from ~ 2.75% p.a. (short-term, 7–45 days) up to ~ 6.60% p.a. (for longer tenures: 2 years and above) (Fi.Money)

- For senior citizens (60+ years): there is a modest premium over general rates — senior FD rates go up to around 7.10% p.a. for long-term tenures (2 years 1 day to 10 years) (Fi.Money)

What Makes ICICI Bank FD a Reliable Option: Benefits & Flexibility

1. Guaranteed/Fixed Returns — Risk Free

The main advantage of a bank FD with ICICI is the certainty: you know the rate when you invest. Your principal remains intact, and returns are not subject to market fluctuations.

2. Flexible Tenures — From Days to Years

ICICI Bank allows a broad array of deposit tenures — from as short as 7 days up to 10 years. This flexibility enables investors to choose based on their horizon: short-term liquidity, medium-term goals, or long-term safety. (Fi.Money)

3. Senior Citizen Advantage

If you are 60 years or older, ICICI gives a premium — roughly 0.5% to 0.75% extra interest — compared to general customers. This makes FDs especially useful for retirees or people seeking stable income. (Fi.Money)

4. Payout Options — Flexibility in Returns

You don’t necessarily have to wait till maturity. ICICI offers options like cumulative FD (interest compounded and paid at maturity) or non-cumulative (monthly/quarterly/annual interest payout). This suits people who need regular income — e.g. retirees, salaried persons wanting interest as supplementary income. (Fi.Money)

5. Low Minimum Deposit and Easy Booking

The minimum amount required is relatively modest (for many FDs, ₹10,000), making FDs accessible even to lower or middle-income investors. (ClearTax) Booking can be done via ICICI’s branches, net banking or mobile banking — making it convenient. (Fi.Money)

6. Option for Premature Withdrawal (with Penalty)

If there’s an emergency, you aren’t completely locked out. ICICI allows premature or partial withdrawal (subject to certain penalty rules), giving liquidity while still offering the safety of a bank deposit. (ICICI Bank)

Things to Keep in Mind (Limitations & What to Watch)

- The interest rates offered by ICICI (and all banks) are not static — they are subject to change. Rates may change based on macroeconomic policy (e.g. variation announced by RBI) and internal bank policy. (ICICI Bank)

- For shorter tenure FDs (few days to few months), the returns are quite modest — sometimes not much more than a savings account, especially after adjusting for inflation.

- Interest earned from FD is taxable. For resident customers, if interest income in a financial year exceeds certain thresholds, TDS may apply. Even without TDS, the interest income is added to your total taxable income. (ICICI Bank)

- With high inflation, real returns (after adjusting for inflation) may be low — especially when interest is ~6–6.5%. So, if inflation is high, the purchasing power may not grow significantly.

- Premature withdrawal carries penalties, which reduce actual returns — so breaking FD before maturity eats into interest income. (ICICI Bank)

- For long-term goals (e.g. retirement after many years), FDs may not beat market-linked investments (equities, mutual funds) over long horizon, though they offer safety and stability.

How to Decide Tenure and FD Strategy with ICICI

Choosing when and how long to invest in FD depends on your financial goal, liquidity needs, and risk appetite. Here are some guiding thoughts:

- Short-term goals or liquidity cushion (less than 6–12 months): opt for short-term FD (e.g. 3–6 months, 6–12 months). Though interest lower, your money stays safe and you avoid locking funds for too long.

- Medium-term goals (1–3 years): Tenures like 1 to 2 years offer a reasonable interest rate (~6.25–6.6%) and moderate commitment.

- Long-term savings with safety (3–10 years): For funds you don’t need immediately (e.g. child’s education after few years, retirement corpus for conservative portion), long-term FD can be a part of the portfolio. Senior citizens will benefit more because of higher rate slabs.

- Regular income flow: If you need periodic income (say monthly/quarterly), opt for non-cumulative FD with monthly/quarterly payout — good for retirees or income supplementers.

- Laddering strategy: Instead of one long FD, you may break funds into multiple FDs with staggered maturities (1-year, 2-year, 3-year) — ensures liquidity at different points and reduces reinvestment risk.

Is ICICI FD Still Competitive — In 2025 Context

Yes — for investors prioritizing safety and stability over high returns or high risk, ICICI Bank FD remains a competitive, reliable instrument:

- The rate range (~2.75%–6.60% for general, ~3.25%–7.10% for senior citizens) is comparable to many banks and reflects prevailing interest environment. (Fi.Money)

- ICICI’s nationwide presence, ease of online booking, trust factor, and flexibility in payout make it suitable for salaried class, retirees, conservative investors or anyone seeking a safe parking for surplus funds.

- For small-to-medium investments or short-to-medium term needs, the lower minimum deposit threshold keeps it accessible.

That said, if an investor’s horizon is very long (10+ years), and they are comfortable with risk, mixing some portion of capital in higher-returning — though volatile — instruments (equity mutual funds, balanced funds, etc.) may yield better inflation-adjusted returns. But for risk-averse investors, FDs with ICICI (or similar banks) have their place in a balanced portfolio.

Frequently Asked Questions (FAQ) — About ICICI Fixed Deposits

Q: What is the minimum amount required to open an FD with ICICI Bank?

A: Typically, the minimum deposit amount is modest (often ₹10,000), which makes it accessible even for small investors. (ClearTax)

Q: For how long can I place an FD with ICICI Bank?

A: ICICI offers flexible tenure options ranging from 7 days to 10 years, giving you the flexibility to match your investment to your time horizon. (Fi.Money)

Q: Is there an option for monthly, quarterly or yearly interest payout?

A: Yes. ICICI allows both cumulative (compounded, paid at maturity) and non-cumulative (monthly/quarterly/annual) payout options — useful for those needing regular income. (Fi.Money)

Q: What if I need my money before maturity — can I break the FD?

A: Yes — ICICI provides a premature withdrawal option, though you may incur a penalty, and interest may be adjusted accordingly. (ICICI Bank)

Q: Are FD interest earnings taxable? What about TDS?

A: Interest on FD is taxable per your income slab. Additionally, if interest from all FDs in a financial year crosses a certain threshold, the bank may deduct TDS at source. For eligible individuals, submitting forms like 15G / 15H may help avoid TDS (though tax still applies). (ICICI Bank)

Q: Is the rate fixed forever once I deposit?

A: The rate is fixed for your deposit’s tenure. However, if you book or renew after maturity, the applicable rate will be as prevailing at that time — which may be higher or lower depending on macroeconomic conditions. (ICICI Bank)

Q: Can NRI/NRO/NRE account holders invest in ICICI FD, and are rates same?

A: Yes — ICICI accepts NRO/NRE FDs. However, certain conditions apply (e.g. NRE FDs have a minimum tenure of 1 year). For domestic/NRO deposits below ₹3 crore, the standard rate slabs apply. (ICICI Bank)

Q: For a retiree or senior citizen — does FD make sense today?

A: Yes — senior citizen rate premium (roughly 0.5%–0.75%) gives a small boost. Combined with safety, flexibility, and regular payout options, FDs remain a dependable component in a conservative retirement income portfolio.

Conclusion — Who Should Consider ICICI FD, and How

If you are someone who values capital safety, predictable income, and liquidity, and you don’t want to risk market volatility, then investing in a fixed deposit with ICICI Bank is a sound decision. It is especially suitable for:

- People pooling funds for short to medium-term needs (1–3 years),

- Retirees or senior citizens seeking stable income,

- Conservative investors looking to park idle cash safely,

- Those who want easy access to funds with minimal risk, and

- Individuals who value flexibility in interest payout (monthly/quarterly) or prefer lump-sum at maturity.

On the other hand, if your horizon is long (10–20 years) and you can tolerate fluctuations, combining FD with higher-return but riskier instruments (equities, funds) would likely outperform after inflation. But as a stable “foundation” in a diversified portfolio, ICICI Bank FD remains relevant.

Leave A Comment

0 Comment